Five Questions to Help Plan for Health Care Costs in Retirement

Posted: March 20, 2025

Updated: March 20, 2025

If you’re planning for retirement, you might be worried about health care costs when you’re no longer covered by your employer. Health care costs can be expensive and complicated. All too often they can dip into retirement savings. According to a joint study between eHealth and Retirable, only about 33% of current retirees and 38% of those currently working set aside funds specifically for health care expenses for the golden years.

Health care has changed over the years with costs increasing steadily for individuals and families. The drivers include a growing demand for expensive medications and an increase in demand for health care services due to an aging population. We are projected to live longer than our parents and grandparents did.

If you’re starting to prepare for health care in retirement, here are five questions to consider.

1. How do you prepare and plan for health care costs in retirement?

Preparing and planning for health care costs in retirement should start many years before it’s time to retire, whether you are self-funding, signing up with Medicare, Medicaid or some form of long-term care coverage. These different approaches are all very complex with pros and cons that are important to understand before making any concrete decisions.

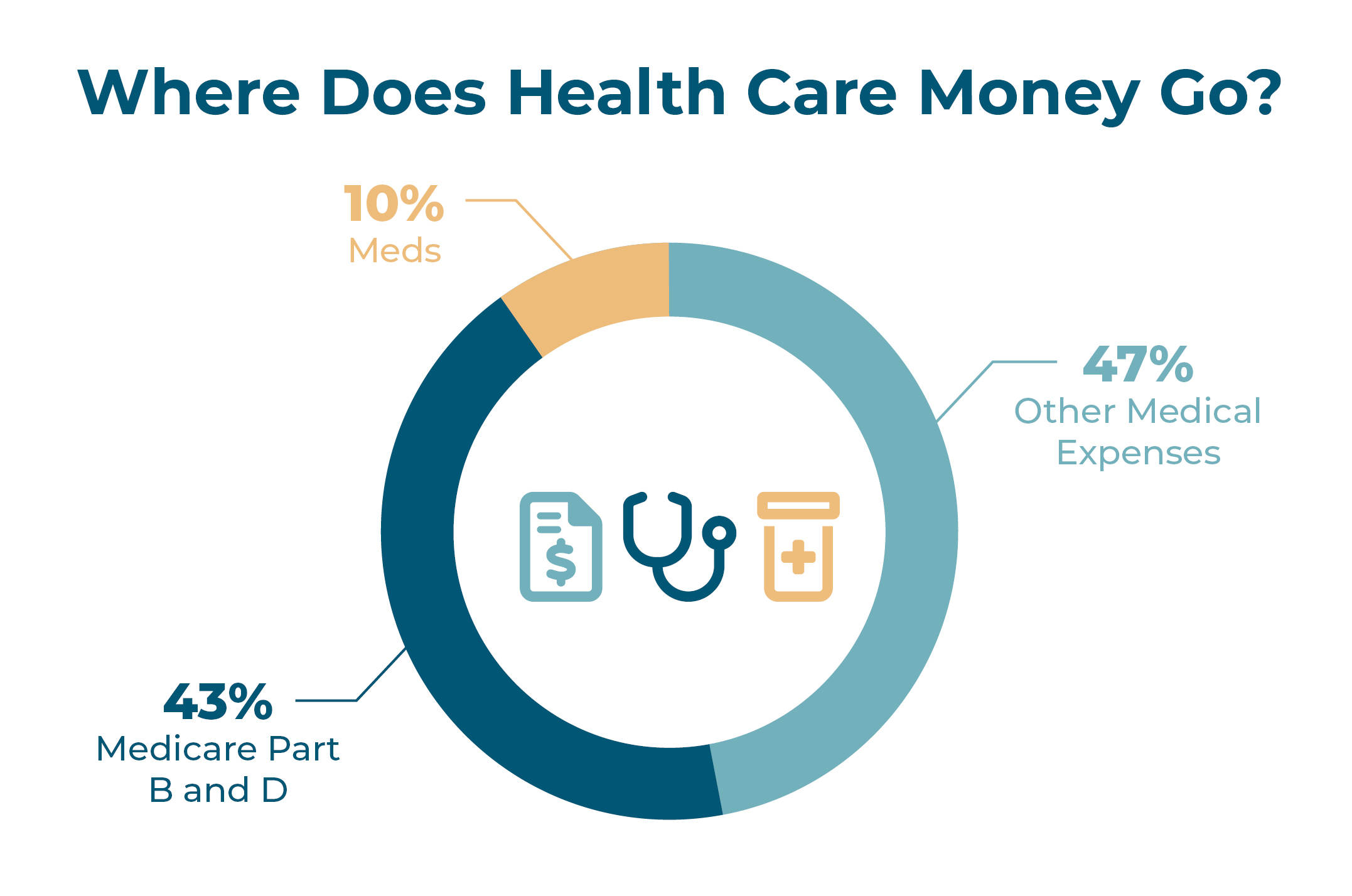

There are strategies you can take to help prepare and plan for the possible health care costs you may face. First, it’s helpful to know where health care money goes. According to Fidelity:

-

43% goes toward Medicare Part B and Part D premiums:

- Doctor appointments and hospital visits

- 10% is put toward medicine

- 47% goes to other medical expenses which include:

- Deductibles for doctor and hospital visits

- Co-payments

- Coinsurance

Here are some strategies you can explore as you look toward the future of health care costs and prepare for the unknown:

- Start saving early, if possible: The more you save, the more your money can grow. If you invest in low-risk options and are patient, compounding will help your savings grow even more.

- Take advantage of your Health Savings Account (HSA): HSAs give you the ability to invest your contributions with any growth on the earnings and interest tax-free. If you begin early enough and allow the money to grow, compounding can also significantly benefit you.

- Lower your modified adjusted gross income (MAGI): Lowering your MAGI has the potential to help reduce health care expenses in the future, particularly Medicare costs. The main reason is that lowering your MAGI can help bypass the financial burden of an Income-Related Monthly Adjustment Amount (IRMAA).

- Don’t forget about long-term care: Having enough money saved for self-funding medical expenses or having a sufficient long-term care insurance policy can greatly help to safeguard your savings in retirement.

2. How much could medical expenses cost me in retirement?

Most retirees aged 65 and older opt for Medicare coverage. Some people get Medicare automatically (Part A), while others have to actively sign up. Generally, it depends if you start getting retirement or disability benefits from Social Security before you turn 65.

You can decline Medicare coverage. However, if you do you may lose your Social Security or Railroad Retirement Board benefits. Plus, you might have to pay a penalty if you decide to enroll later.

For those 65 and up who have Medicare, here are the monthly payments based on income:

- Medicare Part A has no premium; however, you do have a $1,632 deductible in 2025 for each inpatient hospital benefit period before Medicare will begin paying. There is also no limit to the number of benefit periods that can occur in a year meaning you could pay the deductible amount numerous times if you have multiple stays during the year.

The reason this occurs is because the deductible applies to each “benefit period,” which begins when you are admitted to a hospital or skilled nursing facility and ends after you have been released from the facility for 60 consecutive days. Then if you go back to the hospital after those 60 days, a new benefit period begins.

- Medicare Part B has a monthly premium of $185 or higher depending on your income in 2025. The annual deductible for all Medicare Part B beneficiaries will be $257 in 2025. Your monthly premium could be higher depending on these factors:

| Beneficiaries Who File Individual Tax Returns w/ an AGI of | Income-Related Monthly Adjustment (IRMAA) | Total Monthly Premium |

|---|---|---|

| ≤ $106,000 | $0.00 | $185.00 |

| $106,001 – $133,000 | $74.00 | $259.00 |

| $133,001 – $167,000 | $185.00 | $370.00 |

| $167,001 – $200,000 | $295.90 | $480.90 |

| $200,001 – $499,999 | $406.90 | $591.90 |

| ≥ $500,000 | $443.90 | $628.90 |

| Beneficiaries Who File Individual Tax Returns w/ an AGI of | Income-Related Monthly Adjustment (IRMAA) | Total Monthly Premium |

|---|---|---|

| ≤ $212,000 | $0.00 | $185.00 |

| $213,001 – $266,000 | $74.00 | $259.00 |

| $266,001 – $334,000 | $185.00 | $370.00 |

| $334,001 – $400,000 | $295.90 | $480.90 |

| $400,001 – $750,000 | $406.90 | $591.90 |

| ≥ $750,001 | $443.90 | $628.90 |

3. What does Medicare cover and who is eligible?

Medicare covers specified health care services and supplies, depending on your coverage. Medicare does not cover routine physical exams, long-term care, most dental care or eye exams.

- Part A – Hospital Insurance: Inpatient hospital stays, hospice care, certain nursing facility care and some home health care

- Part B – Medical Insurance: Outpatient care, doctors’ services, preventive services and medical supplies

- Part D – Prescription Drug Coverage: Prescription drugs which can be incredibly expensive

For those who don’t carry Medicare in retirement and are no longer working and covered by their employer and earn too much for Medicaid, medical expenses can be significant. Typically, when health issues impact you and you don’t have insurance, out-of-pocket expenses can run up to five times higher than if you had coverage.

You may qualify for free or low-cost health care through Medicaid depending on income and family size. The rules for eligibility differ per state.

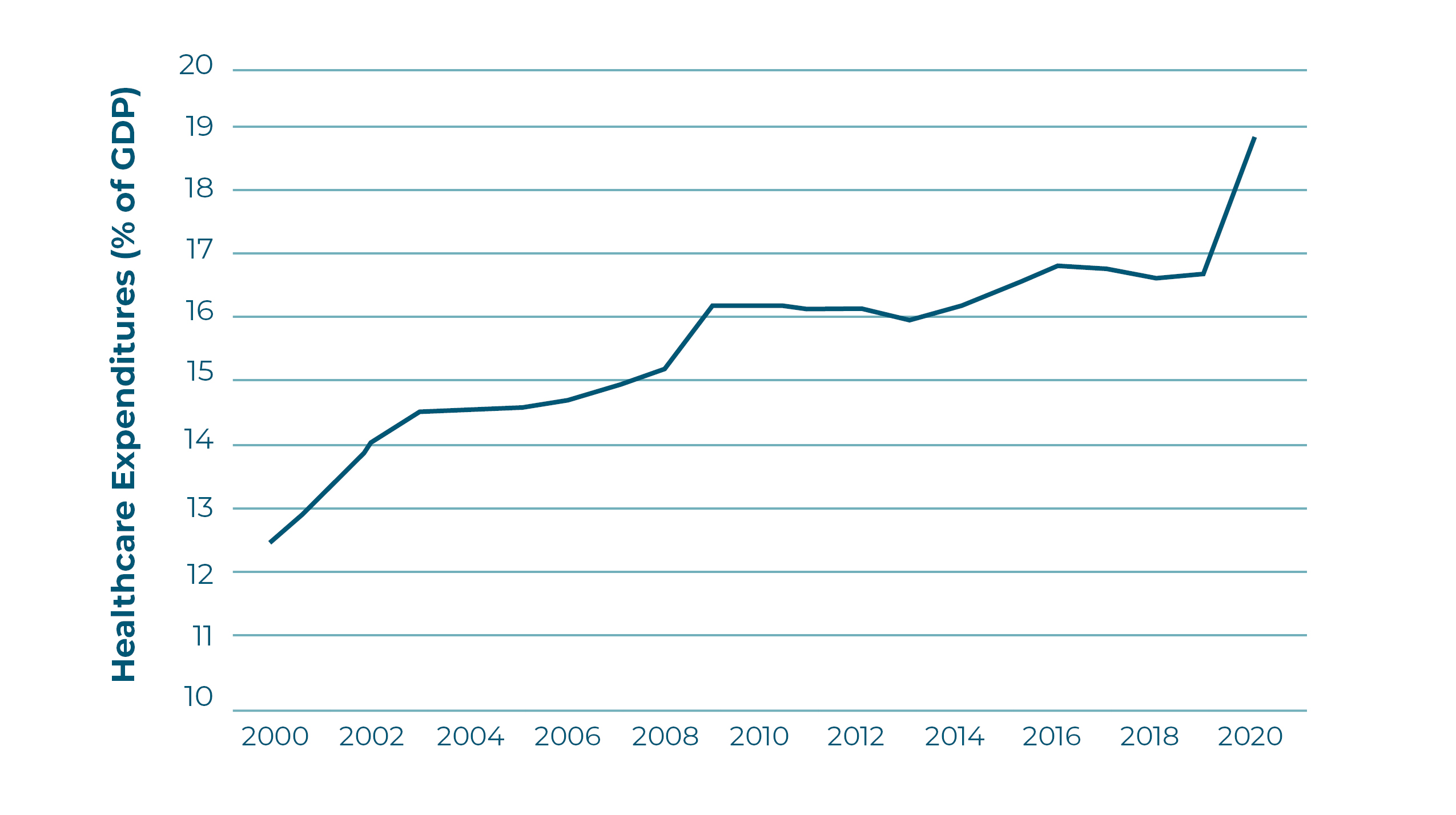

Health care expenditures as a percentage of the U.S. GDP have seen a consistent upward trend. The percentage of GDP that is spent on health care indicates how expensive health care is becoming and is evidence of the importance of having a financial strategy to deal with it when you retire.

2000-2020 Upward Trend of the Increase in Health Care Expenditures

4. What if you retire before you are eligible for Medicare at 65?

If you retire from your job and lose your benefits before 65, you have the option to use the Health Insurance Marketplace to purchase a health care plan. The yearly period of enrollment runs from November 1 through January 15. If you lose the job-based coverage and can’t enroll yet in Medicare, you may qualify for a Special Enrollment Period allowing you to enroll in a health plan outside of the annual Open Enrollment Period.

You could qualify for a Special Enrolment Period if in the past 60 days you or a member of your household experienced one or more of the following:

A loss of, or expects to lose health coverage:

If you or a member of your household lost qualifying health coverage in the last 60 days or expects to lose health care coverage in the next 60 days, you may qualify for a Special Enrollment Period. Also, if you lost Children’s Health Insurance Program (CHIP) coverage or Medicaid, you may qualify for a Special Enrollment Period.

A change within the household:

- Got married

- Had a baby, adopted a child or placed a child through foster care

- Got divorced or legally separated and lost health insurance (Note: Divorce or legal separation without losing your job-based coverage doesn’t qualify you for a Special Enrollment Period)

- Death of someone within your household

A change within the residence:

- If you move to the U.S. from a foreign country or U.S. territory

- If you move to a new home in a new zip code or county

- If you are a student and move from or to the place you attend school

- If you are a seasonal worker and move from or to the place where you both live and work

- If you move from or to a shelter or other transitional housing situation

Traveling for vacation or moving for medical treatment doesn’t qualify you for a Special Enrollment Period. You are required to show that you had qualifying health care coverage for one or more days during the 60 days before your move. However, no proof is needed if you are moving from a foreign country or U.S. territory.

5. What about my future long-term care needs?

Medicare offers quite a bit of medical coverage, about 2/3 of your health care expenses. Although, long-term care is not one of those covered needs. Long-term care can include services like:

- In-Home health care

- Assisted living facilities

- Nursing homes

- Adult day centers

- Occupational, speech, physical and rehab therapies

- Skilled nursing care

- Hospice care

For those who require long-term care, savings can get depleted quickly. According to Morningstar, a mere 8% of the population has some form of long-term care insurance. Long-Term care is often the overlooked aspect of retirement planning that people seem to have the most questions about.

Long-Term care insurance can help safeguard assets and open the door for more choices down the road when and if that time comes for you to receive care. But you don’t want to wait too long to purchase a policy if this is the direction you wish to go. Though there is no official cutoff age for when you can no longer purchase long-term care insurance, but generally most insurance companies won’t issue a new policy for someone between 75 and 80 years old.

What happens if you pay for long-term insurance but never use it?

If you pay long-term care premiums but never actually use the benefits, what happens to them depends on the type of long-term insurance coverage you have. The rules regarding what happens to your benefits are as follows:

- Traditional long-term care insurance

- If you have a policy and die without using it, your beneficiaries won’t receive any benefits

- You pay premiums for life but only receive benefits if you need long-term care

- Hybrid long-term care insurance

- A combination of life insurance and long-term care insurance

- If the benefits of a long-term care insurance policy aren’t used, they transfer to your beneficiaries

- Certain policies allow you to get the entire premium you paid or a portion of it back if you cancel the policy

- Premiums not used and returned to the buyer

- The amount of premium returned depends on how long the policy was held, the buyer’s age, and whether any claims were made against it

- If the policy is canceled, some hybrid policies allow some or all the funds to be returned to the buyer

As life expectancies have increased over the years, so too has the frequency of cognitive decline, and with long-term care premiums continuing to rise, many people are considering self-funding their long-term care.

What is the cost of long-term care with insurance?

As you age there are certain things to consider, one of those is the possibility that you will require long-term care. This would inevitably be an additional expense that would impact your budget; however, for some people, it’s worth it. It’s common for retirees to run out of money due to an unexpected event, such as dealing with a specific illness or having to go into a living assistance facility.

The first step is researching long-term care insurance options and how much such a program costs. The cost of long-term care insurance is influenced by certain factors such as:

- Age

- Health

- Gender

- Marital status

- Policy structure (traditional vs. hybrid policies)

- Location

- Time scale

- Added features

Some of the questions you might have to answer include:

- How old are you? Under 50 or over?

- When do you need coverage? Immediately, within a few weeks or not sure?

- How long do you expect you’ll need coverage for? Less than a year, a year or more, or not sure?

- Have any life events happened that give you a reason to seek new insurance?

- Moved to a new state

- Started or left a job

- Changes to our household

- Lost coverage

- What is your household size?

- How often do you visit a doctor annually?

- Where do you live?

- Do you use tobacco products?

- What is your average yearly household income?

- What is your gender and date of birth?

According to the American Association for Long-Term Care Insurance (AALTCI), the average annual premium for a $165,000-benefit policy with no inflation protection is $950 for a single male (age 55), about $79 per month and $1,500 for a single female (age 55), about $125 per month. For a couple, the combined annual premium is around $2,080.

At retirement age, hovering around 65, a single man would pay an average annual premium of $1,700 annually or a monthly payment of $142. Single women would pay on average, $2,700 annually, which is about $225 per month.

These standard estimated numbers are recognized by the AALTCI and the National Council on Aging (NCOA) as a benchmark that can help you determine your own situation and create strategies to safeguard your assets.

What is the cost of long-term care without insurance?

Private health insurance, including Medicare, does not pay for long-term care. In some cases, Medicaid will help but it would require depleting a significant amount of savings to become eligible, and Medicaid coverage also requires participants to select from approved long-term facilities. Monthly costs of assisted living arrangements can range anywhere from $4,000 to nearly $15,000 per month.

Some of the long-term care alternatives that you can consider include:

- Self-Funding: You can pay out-of-pocket

- Medicaid: If you qualify

- Hybrid life insurance: This approach pays out a death benefit and covers long-term care

- Selling assets to cover the bills: If you have to relocate to a facility, you can decide if it is beneficial to sell your home or other items of value to help cover the costs

- Obtaining a home equity loan: Securing a loan is another approach that may work for you and your retirement goals

Where can I buy long-term insurance?

If you are interested in long-term care insurance, you can purchase it from a licensed insurance agent, financial professional or broker. If you are still employed, long-term care insurance might be an option through your employer.

In some cases, you can purchase a shorter-term policy through a state partnership program. If you go this route and exhaust all your benefits, you then may qualify for Medicaid coverage, or you can self-fund.

Meet With a Financial Professional

Taking action is the first step toward safeguarding your assets and creating a strategy to prepare for health care in retirement. Reach out to us today to schedule a consultation to discuss your options. We’ll work with you to craft a plan to help you work towards your financial goals in retirement.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

The LPL Financial registered representatives associated with this website may discuss and/or transact business only with residents of the states in which they are properly registered or licensed. No offers may be made or accepted from any resident of any other state.

Landmark Credit Union ("Financial Institution") provides referrals to financial professionals of LPL Financial LLC pursuant to an agreement that allows LPL to pay the Financial Institution for these referrals. This creates an incentive for the Financial Institution to make these referrals, resulting in a conflict of interest. The Financial Institution is not a current client of LPL for advisory services. Please visit https://www.lpl.com/disclosures/is-lpl-relationship-disclosure.html

Securities and advisory services are offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. Landmark Credit Union and Landmark Investment Center are not registered as a broker-dealer or investment advisor. Registered representatives of LPL offer products and services using Landmark Investment Center, and may also be employees of Landmark Credit Union. These products and services are being offered through LPL or its affiliates, which are separate entities from, and not affiliates of, Landmark Credit Union or Landmark Investment Center. Securities and insurance offered through LPL or its affiliates are:

| Not Insured by NCUA or Any Other Government Agency | Not Landmark Credit Union Guaranteed | Not Landmark Credit Union Deposits or Obligations | May Lose Value |